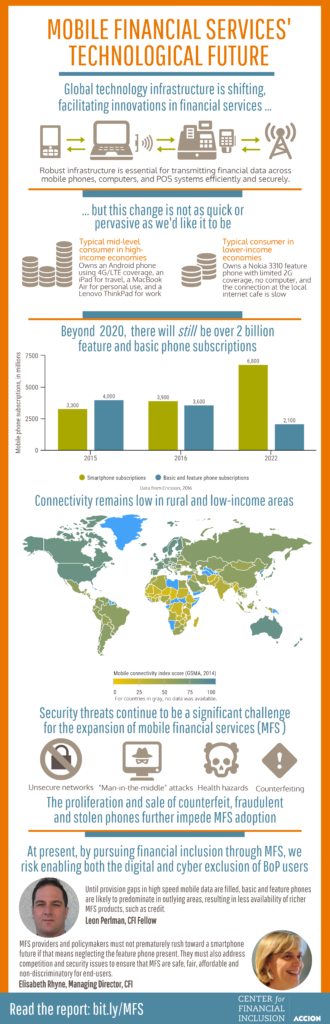

Since the debut of mobile financial services (MFS) 10 years ago, the sector is now preparing for a switch to smartphones that will enable even more and better services. Not so fast, cautions CFI Fellow Leon Perlman.

In his report, Technology Inequality: Opportunities and Challenges for Mobile Financial Services, Perlman steers readers through a primer on the technology that enables MFS to operate on basic, feature and smart phones. But more importantly, the report sounds a cautionary note about the readiness of the sector for a large-scale shift to smartphone and internet-based MFS, particularly for low-end consumers. Leon’s on-the-ground research conducted in 12 different countries finds that smartphone-enabled MFS is not an impending panacea for financial inclusion. Due to the slow spread of reliable, high-quality 3G coverage and sufficiently capable smartphones, the majority of MFS will be accessed on feature phones, using Unstructured Supplementary Service Data (USSD), SIM Application Toolkit (STK) and java-applets, rather than internet-enabled smartphones, for the forseeable future.

This report urges regulators and technology providers to continue supporting MFS based on feature phones, even as they work to create paths for new-generation services. While smartphones promise more intuitive and richer user interfaces, this promise will take some time to materialize fully and robustly. If mobile financial services are to be a force for financial inclusion, we must not prematurely abandon older technologies as we concurrently push to create a smartphone-based future.

Major Findings

Major Findings

- For MFS to continue to grow, it is important to continue supporting feature phones with USSD and STK interfaces.

MFS, for people at the base of the economic pyramid (BoP), are currently provided largely on feature phones operating across 2G mobile networks and using menu-driven, text-based user interfaces. The main technologies facilitating MFS here are Unstructured Supplementary Service Data (USSD),Short Message Service (SMS) in its SIM Application Toolkit (STK) incarnation, and Java applets.Feature phones are likely to dominate MFS for BoP for the foreseeable future. While smartphones are penetrating BoP markets, the pace remains relatively slow. Additonally, feature phone manufacturing is actually growing. As early mobile technology patents expire, feature phone costs will continue to drop and use will grow. - Realizing the promise of smartphones for MFS first requires improving their technical specifications and the presence of high-speed networks. Cheap smartphones are not yet sophisticated enough to support MFS. Gaps in high-speed 3G mobile data coverage persist, especially in MFS-focused rural and peri-urban areas. Where there is no 3G coverage, there is usually no 4G coverage either. While 3G (and 4G) coverage is predominant in urban areas and along major highways, rural areas still receive mainly 2G coverage.

- Costs, for both customers and providers, are the source of many of constraints to smartphone MFS adoption. Data costs for data-hungry smartphones may be prohibitive for many BoP users. Manufacturers produce less sophisticated phones to keep prices affordable for the mass market. Mobile network operators (MNOs) face high costs for acquiring spectrum and building infrastructure in rural areas in order to expand and upgrade service.

- Security vulnerabilities on MFS channels and devices put customer transactions and MFS systems at risk. The 1970s-era Signaling System 7 (SS7) technology that enables mobile phone (and landline) communications is not secure and has been exploited by bad actors for decades. The standard mobile air platform is susceptible to relatively cheap, homemade devices performing “man-in-the-middle” interception of mobile voice, SMS and data traffic. Counterfeit and stolen phone sales are increasing and some MFS smartphone apps are designed with insufficient security. On the brighter side, MFS apps on feature phones and written in Java mostly use encrypted SMS, so they could provide a secure and ubiquitous means of transacting.

- Policy makers must address competition issues for MFS systems. Access to service gateways should be fair, reasonable and non-discriminatory. MNOs may be gatekeepers for access to services and infrastructure for competing MFS providers. Those competing service providers may be handicapped (“foreclosed”) by being denied access to USSD or STK gateways and short codes or through prohibitive pricing. Also, MNOs and non-bank service providers may be denied access to payment infrastructures required to interoperate or provide services such as merchant acceptance or ATM withdrawals. Thin SIM technology is being implemented in several countries as a technical fix to evade such blockages.

Explore More